💸 Why Your Cost of Living Is Not Going Back to “Normal”

Patrick Boyle’s latest video focuses on a brutal but important economic reality: even when inflation slows down, prices usually do not return to where they were before.

That is the part many people misunderstand.

Inflation going from 8% to 2% does not mean life becomes cheap again. It means prices are still rising, just more slowly. The previous price increases remain embedded in rent, groceries, insurance, services, restaurants, and daily expenses.

📉 Lower inflation ≠ lower prices.

This is why many people still feel poorer even after official inflation numbers improve.

The deeper issue is that wages often recover slowly, while essential costs adjust quickly and rarely reverse. Housing, food, energy, healthcare, transportation, and insurance became structurally more expensive after the pandemic inflation shock. In many countries, real wages are now recovering, but OECD data still shows that in half of OECD countries real wages remained below early-2021 levels as of Q1 2025.

So the “cost of living crisis” is not only about inflation today. It is about the permanent price level left behind by past inflation.

Light deep dive:

There are three layers to the problem.

1️⃣ First, prices are sticky. Companies are usually quicker to raise prices than to cut them. Once consumers accept a new price level, businesses have little incentive to reverse it unless demand collapses or competition forces them.

2️⃣ Second, essential goods hit harder. A 20% increase in luxury goods is optional. A 20% increase in rent, food, energy, or insurance directly reduces disposable income.

3️⃣ Third, asset owners and wage earners experience inflation differently. People who own property, stocks, or businesses may see nominal wealth rise. People relying mainly on wages feel the pressure first, because their income adjusts later and often incompletely.

➡️ The result is a strange economy where headline indicators can look stable while households still feel squeezed.

The big takeaway:

Inflation can come down.

Interest rates can stabilize.

Markets can recover.

But unless wages grow faster than prices for long enough, the standard of living does not fully recover.

That is why the cost of living debate is becoming one of the most important economic issues of the decade.

Source:

📱 Patrick Boyle

Supporting data:

🔗 OECD real wages recovering but still below early-2021 levels in half of OECD countries

🔗 IMF global inflation trend and macroeconomic outlook

🔗 World Bank cost of living pressures remain elevated in several economies

Patrick Boyle’s latest video focuses on a brutal but important economic reality: even when inflation slows down, prices usually do not return to where they were before.

That is the part many people misunderstand.

Inflation going from 8% to 2% does not mean life becomes cheap again. It means prices are still rising, just more slowly. The previous price increases remain embedded in rent, groceries, insurance, services, restaurants, and daily expenses.

This is why many people still feel poorer even after official inflation numbers improve.

The deeper issue is that wages often recover slowly, while essential costs adjust quickly and rarely reverse. Housing, food, energy, healthcare, transportation, and insurance became structurally more expensive after the pandemic inflation shock. In many countries, real wages are now recovering, but OECD data still shows that in half of OECD countries real wages remained below early-2021 levels as of Q1 2025.

So the “cost of living crisis” is not only about inflation today. It is about the permanent price level left behind by past inflation.

Light deep dive:

There are three layers to the problem.

The big takeaway:

The economy may “normalize” statistically, but your personal budget may not.

Inflation can come down.

Interest rates can stabilize.

Markets can recover.

But unless wages grow faster than prices for long enough, the standard of living does not fully recover.

That is why the cost of living debate is becoming one of the most important economic issues of the decade.

Source:

Supporting data:

Please open Telegram to view this post

VIEW IN TELEGRAM

YouTube

Is Inflation About to Get Much Worse?

🚀 Streamline your entire business with Odoo — the all-in-one, easy-to-use ERP platform that centralizes, automates, and scales your operations from sales and accounting to inventory and eCommerce 📈⚙️. Try out Odoo for 15 days (no credit card required) 👉🏻…

❤1

Forwarded from Finance facts 💼

What does GDP stand for?

Anonymous Quiz

76%

Gross Domestic Product

13%

Gross Demand Pricing

7%

General Domestic Profit

5%

Global Debt Position

This week is relatively light early on due to multiple global holidays, but key US macro data later in the week could drive markets — especially around growth, labor, and inflation.

🧠 Early week: low liquidity, central bank focus

Monday–Tuesday are impacted by holidays across major economies (Japan, China, UK), meaning:

👉 thinner trading volumes

👉 potentially higher volatility on low activity

The main early catalyst:

• 🇦🇺 RBA Rate Decision

Expected at 4.35% (vs 4.10%)

👉 Signals continued tightening bias

📊 Midweek: growth & demand signals (US)

Markets will focus on services and labor demand:

• Services PMI / ISM Services

→ Expected stable (~51–54 range)

👉 Indicates moderate expansion

• JOLTS Job Openings

→ Slight decline expected

👉 Cooling labor demand

• ADP Employment (Wed)

→ Expected ~90K (vs 62K prior)

👉 Early signal for payrolls

🛢 Energy market check

• Crude Oil Inventories (Wed)

👉 Key for oil price direction and inflation expectations

📉 Late week: labor market in focus (KEY EVENT)

Friday is the most important day:

• Nonfarm Payrolls (NFP)

→ Expected: 73K (vs 178K prior)

👉 Significant slowdown

• Unemployment Rate

→ Expected: 4.3% (stable)

• Wage Growth (MoM)

→ Expected: 0.3% (vs 0.2%)

👉 Markets will watch the balance between:

• slowing job growth

• still-solid wages

💡 Key insight

This week is about one question:

👉 Is the US labor market cooling enough to justify rate cuts?

• Weak jobs → bullish for markets (rate cuts)

• Strong wages → inflation risk remains

📝 In brief

• Early week → low liquidity

• Midweek → growth + demand signals

• Friday → critical labor market data

👉 Expect volatility around NFP

#Macro #EconomicCalendar #NFP #Markets #Finance

Please open Telegram to view this post

VIEW IN TELEGRAM

👍2

Please open Telegram to view this post

VIEW IN TELEGRAM

🛢The End of the Petro-Dollar?💵

For decades, the petrodollar has been one of the biggest pillars of U.S. financial power 🇺🇸

The basic idea was simple:

🌍 Oil was mostly priced and traded in U.S. dollars.

🏦 Oil-exporting countries earned dollars.

📈 Those dollars were often recycled into U.S. financial assets, especially Treasuries.

That created constant global demand for the dollar.

If a country wanted oil, it needed dollars.

If oil exporters earned dollars, they often reinvested them into U.S. markets.

That cycle helped strengthen the dollar’s role as the world’s reserve currency.

But now, that system is under pressure⚠️

🇨🇳 China is pushing more trade in yuan.

🇷🇺 Russia is avoiding dollar-based payment systems.

🧱 BRICS countries are discussing alternative settlement mechanisms.

🛢 Gulf countries are selling more energy to Asia.

🇺🇸 And the U.S. is now far less dependent on Middle Eastern oil than it was in the 1970s.

So the question is not:

“Will the dollar collapse tomorrow?” ❌

That is too simplistic.

The real question is:

“Is the global financial system slowly becoming more multipolar?” 🌐

🔍 Light deep dive:

The petrodollar system was never just about oil.

It was about power.

🛢 Energy trade supported dollar demand.

💵 Dollar demand supported U.S. borrowing capacity.

🏛 U.S. borrowing capacity supported military and geopolitical influence.

🌍 That influence reinforced the global role of the dollar.

It was a self-reinforcing loop 🔁

But loops can weaken.

If more countries settle trade in local currencies, if oil exporters diversify their reserves, and if geopolitical rivals build alternative payment rails, the dollar may remain dominant while gradually losing some of its monopoly power.

That is the key distinction.

The dollar does not need to “die” for the petrodollar system to weaken.

It only needs to become less central.

📊 For investors, this matters because a weaker petrodollar structure could affect:

• demand for U.S. Treasuries 🏦

• long-term U.S. borrowing costs 📈

• commodity pricing 🛢

• emerging market currency strategy 🌍

• geopolitical risk premiums ⚔️

• gold and alternative reserve assets 🥇

• the role of China and the yuan in global trade 🇨🇳

The most realistic scenario is not a sudden collapse.

More dollar trade.

More yuan trade.

More bilateral settlements.

More gold accumulation.

More financial blocs.

The world may be moving from one dominant monetary empire to a messier, multipolar system 🌐

And that could be one of the biggest macro shifts of the next decade.

Source video:

📱 The End Of The Petro-Dollar

Additional sources:

🔗 Council on Foreign Relations — Petrodollars: Myth and Reality

🔗 Atlantic Council — Is the end of the petrodollar near?

🔗 Investopedia — Petrodollars and the U.S. Dollar

#️⃣ #️⃣ #️⃣

#Finance #Economics #Petrodollar #USDollar #Oil #Macro #Geopolitics #BRICS #China #Gold #Treasuries #GlobalMarkets #Investing

For decades, the petrodollar has been one of the biggest pillars of U.S. financial power 🇺🇸

The basic idea was simple:

🌍 Oil was mostly priced and traded in U.S. dollars.

🏦 Oil-exporting countries earned dollars.

That created constant global demand for the dollar.

If a country wanted oil, it needed dollars.

If oil exporters earned dollars, they often reinvested them into U.S. markets.

That cycle helped strengthen the dollar’s role as the world’s reserve currency.

But now, that system is under pressure

🇨🇳 China is pushing more trade in yuan.

🇷🇺 Russia is avoiding dollar-based payment systems.

🧱 BRICS countries are discussing alternative settlement mechanisms.

🛢 Gulf countries are selling more energy to Asia.

🇺🇸 And the U.S. is now far less dependent on Middle Eastern oil than it was in the 1970s.

So the question is not:

“Will the dollar collapse tomorrow?” ❌

That is too simplistic.

The real question is:

“Is the global financial system slowly becoming more multipolar?” 🌐

The petrodollar system was never just about oil.

It was about power.

🛢 Energy trade supported dollar demand.

💵 Dollar demand supported U.S. borrowing capacity.

🏛 U.S. borrowing capacity supported military and geopolitical influence.

🌍 That influence reinforced the global role of the dollar.

It was a self-reinforcing loop 🔁

But loops can weaken.

If more countries settle trade in local currencies, if oil exporters diversify their reserves, and if geopolitical rivals build alternative payment rails, the dollar may remain dominant while gradually losing some of its monopoly power.

That is the key distinction.

The dollar does not need to “die” for the petrodollar system to weaken.

It only needs to become less central.

📊 For investors, this matters because a weaker petrodollar structure could affect:

• demand for U.S. Treasuries 🏦

• long-term U.S. borrowing costs 📈

• commodity pricing 🛢

• emerging market currency strategy 🌍

• geopolitical risk premiums ⚔️

• gold and alternative reserve assets 🥇

• the role of China and the yuan in global trade 🇨🇳

The most realistic scenario is not a sudden collapse.

It is fragmentation 🧩

More dollar trade.

More yuan trade.

More bilateral settlements.

More gold accumulation.

More financial blocs.

The world may be moving from one dominant monetary empire to a messier, multipolar system 🌐

And that could be one of the biggest macro shifts of the next decade.

Source video:

Additional sources:

#Finance #Economics #Petrodollar #USDollar #Oil #Macro #Geopolitics #BRICS #China #Gold #Treasuries #GlobalMarkets #Investing

Please open Telegram to view this post

VIEW IN TELEGRAM

YouTube

The End Of The Petro-Dollar

UAE Leaves OPEC, China Wins

► Go to https://ground.news/jikh to access world-wide perspectives in one place, compare coverage, and stay fully informed on our economy and more. Subscribe for 40% off unlimited access through my link

► Premium Membership (extra…

► Go to https://ground.news/jikh to access world-wide perspectives in one place, compare coverage, and stay fully informed on our economy and more. Subscribe for 40% off unlimited access through my link

► Premium Membership (extra…

❤6🔥2👏2👍1🎉1

Germany is facing a demographic collapse that threatens its status as one of the world's richest nations. For over 55 years, fertility rates have remained below the replacement level, currently sitting at 1.4 children per woman.

This isn't just about "fewer people" it's a fundamental shift in population composition. By 2026, Germany has become one of the oldest countries globally, with a median age over 45. Almost 40% of the population is over 50, while only 1 in 8 is a child under 14.

The "generational contract" is tearing up: the systems built for a young, growing workforce cannot simply be downscaled to support a rapidly aging society.

The "Baby Boomer" mismanagement has left younger generations (Millennials and Gen Z) with an impossible math problem. By 2036, 13 million boomers will retire, leaving millions of jobs unfilled and a shrinking tax base to fund the welfare state.

Germany’s "pay-as-you-go" pension system is hitting a breaking point. In the 1960s, there were five workers for every retiree; by the 2030s, that ratio will drop to 2:1.

Currently, the federal government already spends roughly 25% of its annual tax revenue just to plug holes in the pension system more than it spends on education, infrastructure, and defense combined.

This creates a massive redistribution of wealth from the young and working to the old and retired, leaving little capital for investments that could help young families, such as affordable housing or childcare.

Young Germans face some of the highest tax burdens in the world (up to 50%), making it nearly impossible to save for their own future or afford homes in metropolitan areas where housing supply is far behind demand.

While immigration has delayed the crash, it is not a permanent solution. To keep the population stable, Germany would need a constant influx of new immigrants, but birth rates are crashing globally.

The world is "running out of young people," meaning competition for workers will intensify. Furthermore, immigrants' birth rates tend to align with the local population within two generations, meaning they too will eventually require a new generation of workers to support their retirement.

Solving this crisis requires "intensely unpopular" political choices: shifting funds from the wealthy elderly to young families. Without radical change, the German welfare state and living standards are on a path toward a significant decline.

#Germany #Demographics #Economy #FutureOfWork #PensionCrisis #GlobalTrends #SocialCollapse #Europe #Economics #PopulationCrash

Please open Telegram to view this post

VIEW IN TELEGRAM

YouTube

GERMANY IS OVER

Do you have a balanced news diet? Go to https://ground.news/nutshell to see reporting from a variety of sources and perspectives around the world. Subscribe for 40% off their unlimited access Vantage plan through our link.

Support independent science and…

Support independent science and…

❤5👍4🔥4🎉4💯4

🔵 Cross Promotion 🔵

➖➖➖➖➖➖➖➖

📢 Revolutionary Talk </>

ℹ️ Geopolitical News channel

👉 @Revolutionary_Talk

📢 🔰 GCI Sikar™ 🔰

ℹ️ Lectur

👉 @GCI_CLC_Allen_PCP_Sikar_Lectures

📢 Aᴍᴏʀ ᴇɴᴛᴇʀᴛᴀɪɴᴍᴇɴᴛ™️

ℹ️ Stream all movies and series

👉 @allmovies_site

📢 Positive vibes

ℹ️ ❤️Positive QuOtes❤️

👉 @positivevibes_s

📢 🍳 The Flavor Corner

ℹ️ Delicious recepies

👉 @best_recepies

📢 🤍 𝐇𝐞𝐚𝐫𝐭 𝐓𝐨𝐮𝐜𝐡 !! मोहब्बत शायरी 🌸

ℹ️ मोहब्बत शायरी

👉 @Shayari_Expert

📢 Hoops Hype Room 🏀

ℹ️ Basketball channel

👉 @basket_updates

📢 Your Inner voice

ℹ️ Think smarter, stress less, win🚀

👉 @life_changing_quote

📢 CricFreak

ℹ️ Latest Cricket Updates

👉 @cricfreakk

📢 𝐃𝐀𝐈𝐋𝐘 𝐂𝐔𝐑𝐑𝐄𝐍𝐓 𝐄𝐕𝐄𝐍𝐓𝐒

ℹ️ Daily National & International News

👉 @dailycurrentevents

📢 🔮PULSE

ℹ️ Viral videoss😍

👉 @pulse_viral

#free #ads #boost

➖➖➖➖➖➖➖➖

➖➖➖➖➖➖➖➖

📢 Revolutionary Talk </>

ℹ️ Geopolitical News channel

👉 @Revolutionary_Talk

📢 🔰 GCI Sikar™ 🔰

ℹ️ Lectur

👉 @GCI_CLC_Allen_PCP_Sikar_Lectures

📢 Aᴍᴏʀ ᴇɴᴛᴇʀᴛᴀɪɴᴍᴇɴᴛ™️

ℹ️ Stream all movies and series

👉 @allmovies_site

📢 Positive vibes

ℹ️ ❤️Positive QuOtes❤️

👉 @positivevibes_s

📢 🍳 The Flavor Corner

ℹ️ Delicious recepies

👉 @best_recepies

📢 🤍 𝐇𝐞𝐚𝐫𝐭 𝐓𝐨𝐮𝐜𝐡 !! मोहब्बत शायरी 🌸

ℹ️ मोहब्बत शायरी

👉 @Shayari_Expert

📢 Hoops Hype Room 🏀

ℹ️ Basketball channel

👉 @basket_updates

📢 Your Inner voice

ℹ️ Think smarter, stress less, win🚀

👉 @life_changing_quote

📢 CricFreak

ℹ️ Latest Cricket Updates

👉 @cricfreakk

📢 𝐃𝐀𝐈𝐋𝐘 𝐂𝐔𝐑𝐑𝐄𝐍𝐓 𝐄𝐕𝐄𝐍𝐓𝐒

ℹ️ Daily National & International News

👉 @dailycurrentevents

📢 🔮PULSE

ℹ️ Viral videoss😍

👉 @pulse_viral

#free #ads #boost

➖➖➖➖➖➖➖➖

🔵 Cross Promotion 🔵

➖➖➖➖➖➖➖➖

📢 Aᴍᴏʀ ᴇɴᴛᴇʀᴛᴀɪɴᴍᴇɴᴛ™️

ℹ️ Stream all movies and series

👉 @allmovies_site

📢 🔰 GCI Sikar™ 🔰

ℹ️ Lectur

👉 @GCI_CLC_Allen_PCP_Sikar_Lectures

📢 Revolutionary Talk </>

ℹ️ Geopolitical News channel

👉 @Revolutionary_Talk

📢 🔮PULSE

ℹ️ Viral videoss😍

👉 @pulse_viral

📢 𝐃𝐀𝐈𝐋𝐘 𝐂𝐔𝐑𝐑𝐄𝐍𝐓 𝐄𝐕𝐄𝐍𝐓𝐒

ℹ️ Daily National & International News

👉 @dailycurrentevents

📢 Your Inner voice

ℹ️ Think smarter, stress less, win🚀

👉 @life_changing_quote

📢 Hoops Hype Room 🏀

ℹ️ Basketball channel

👉 @basket_updates

📢 🤍 𝐇𝐞𝐚𝐫𝐭 𝐓𝐨𝐮𝐜𝐡 !! मोहब्बत शायरी 🌸

ℹ️ मोहब्बत शायरी

👉 @Shayari_Expert

📢 🍳 The Flavor Corner

ℹ️ Delicious recepies

👉 @best_recepies

📢 Positive vibes

ℹ️ ❤️Positive QuOtes❤️

👉 @positivevibes_s

#free #ads #boost

➖➖➖➖➖➖➖➖

➖➖➖➖➖➖➖➖

📢 Aᴍᴏʀ ᴇɴᴛᴇʀᴛᴀɪɴᴍᴇɴᴛ™️

ℹ️ Stream all movies and series

👉 @allmovies_site

📢 🔰 GCI Sikar™ 🔰

ℹ️ Lectur

👉 @GCI_CLC_Allen_PCP_Sikar_Lectures

📢 Revolutionary Talk </>

ℹ️ Geopolitical News channel

👉 @Revolutionary_Talk

📢 🔮PULSE

ℹ️ Viral videoss😍

👉 @pulse_viral

📢 𝐃𝐀𝐈𝐋𝐘 𝐂𝐔𝐑𝐑𝐄𝐍𝐓 𝐄𝐕𝐄𝐍𝐓𝐒

ℹ️ Daily National & International News

👉 @dailycurrentevents

📢 Your Inner voice

ℹ️ Think smarter, stress less, win🚀

👉 @life_changing_quote

📢 Hoops Hype Room 🏀

ℹ️ Basketball channel

👉 @basket_updates

📢 🤍 𝐇𝐞𝐚𝐫𝐭 𝐓𝐨𝐮𝐜𝐡 !! मोहब्बत शायरी 🌸

ℹ️ मोहब्बत शायरी

👉 @Shayari_Expert

📢 🍳 The Flavor Corner

ℹ️ Delicious recepies

👉 @best_recepies

📢 Positive vibes

ℹ️ ❤️Positive QuOtes❤️

👉 @positivevibes_s

#free #ads #boost

➖➖➖➖➖➖➖➖

🍏 Apple Eyes Intel & Samsung for Future Chip Supply

Apple is reportedly in early-stage talks with Intel and Samsung to potentially supply main processors for its devices.

This would be a major strategic shift.

For years, Apple has relied heavily on TSMC for its most advanced chips. But rising geopolitical risk around Taiwan, trade tensions, and AI-driven chip bottlenecks are forcing Big Tech to rethink supply chains.

Why it matters:

• Apple could reduce dependence on Taiwan

• Intel and Samsung could gain one of the world’s most valuable chip customers

• The move would support US and South Korean semiconductor manufacturing

• It may strengthen Intel’s comeback narrative after years of execution problems

Intel shares jumped sharply after the news, showing how powerful an Apple partnership could be for investor sentiment.

Still, the talks are preliminary. No orders have been placed yet, and Apple could still walk away.

📌 Market takeaway:

This is not just about Apple. It is about the next phase of the global semiconductor war: AI demand, supply-chain security, and geopolitical hedging.

Source: Bloomberg

#️⃣ #️⃣ #️⃣

#Apple #Intel #Samsung #TSMC #Semiconductors #AIChips #BigTech #StockMarket #Investing #Finance

Apple is reportedly in early-stage talks with Intel and Samsung to potentially supply main processors for its devices.

This would be a major strategic shift.

For years, Apple has relied heavily on TSMC for its most advanced chips. But rising geopolitical risk around Taiwan, trade tensions, and AI-driven chip bottlenecks are forcing Big Tech to rethink supply chains.

Why it matters:

• Apple could reduce dependence on Taiwan

• Intel and Samsung could gain one of the world’s most valuable chip customers

• The move would support US and South Korean semiconductor manufacturing

• It may strengthen Intel’s comeback narrative after years of execution problems

Intel shares jumped sharply after the news, showing how powerful an Apple partnership could be for investor sentiment.

Still, the talks are preliminary. No orders have been placed yet, and Apple could still walk away.

This is not just about Apple. It is about the next phase of the global semiconductor war: AI demand, supply-chain security, and geopolitical hedging.

Source: Bloomberg

#Apple #Intel #Samsung #TSMC #Semiconductors #AIChips #BigTech #StockMarket #Investing #Finance

Please open Telegram to view this post

VIEW IN TELEGRAM

The Daily Upside

Apple Flirts With Adding Intel, Samsung into Main Chip Supply Chain

Apple’s supply chain and manufacturing dependencies have turned problematic in the age of tariffs and friend-shoring.

👍5👏4💯4❤3🔥3🎉2

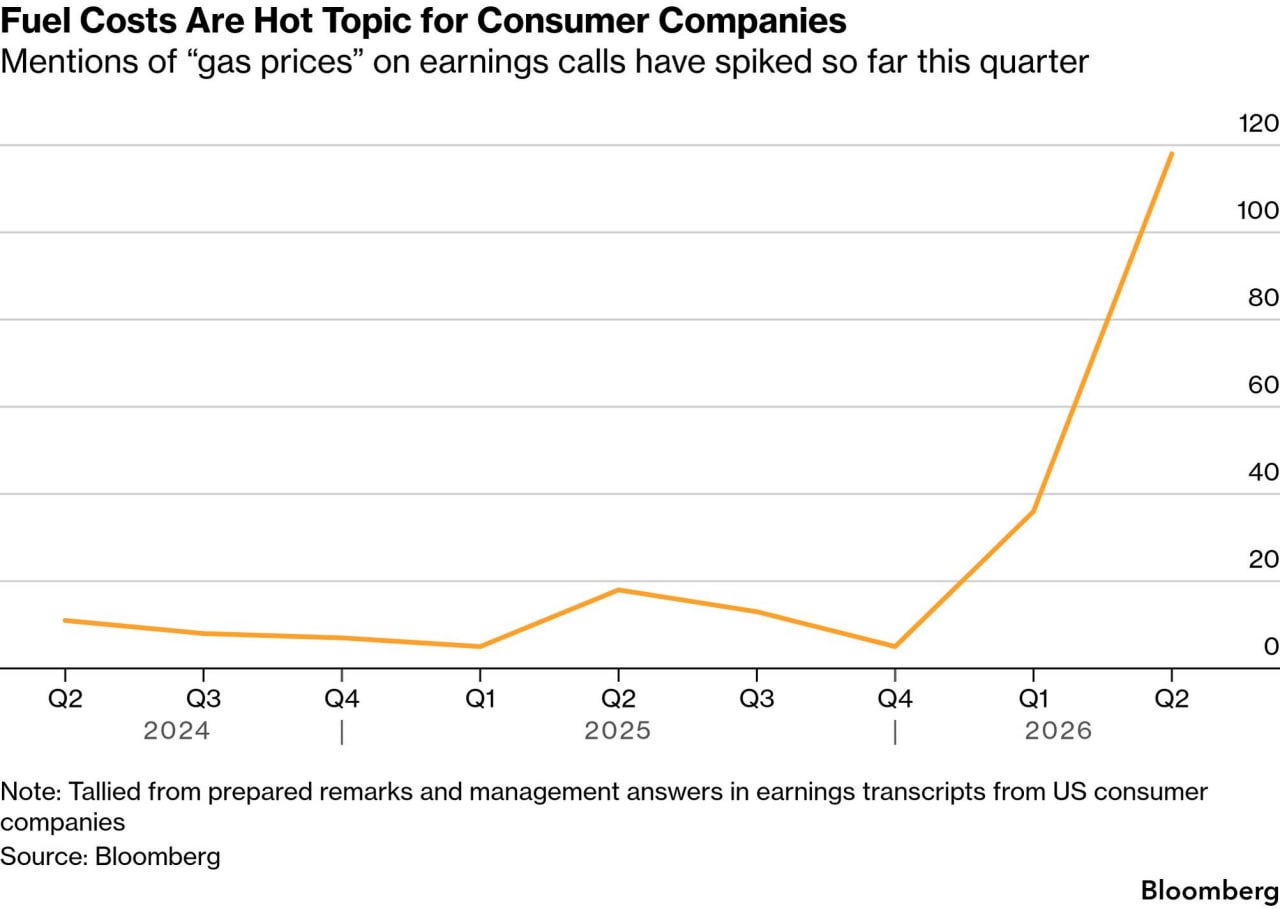

⛽️Iran War Sends Gas Prices to 2022 Highs

The economic impact of the Iran war is now hitting American consumers directly at the pump.

US gasoline prices have climbed to around $4.56 per gallon, the highest level since July 2022, according to AAA data reported by Investopedia. Prices have risen for 15 consecutive days, jumping roughly 54 cents since April 22.

The pressure is not just on drivers.

Higher fuel costs act like a hidden tax on the economy: consumers spend more on gas, leaving less money for restaurants, retail, travel, and discretionary purchases.

📌 Why it matters:

• Higher gas prices can weaken consumer spending

• Transport and logistics costs may rise

• Inflation pressure could remain sticky

• Businesses dependent on discretionary spending may feel the squeeze

• Oil and energy stocks could benefit, while consumer-facing sectors face pressure

The conflict is also affecting global oil markets and shipping risk, especially around the Strait of Hormuz, one of the world’s most important energy chokepoints. AP reported fresh military tensions involving Iranian attacks on US Navy ships in the Strait of Hormuz, adding another layer of risk to energy markets.

📉 Market takeaway:

This is bigger than expensive gas.

If energy prices stay elevated, the Iran war could become a macro problem: weaker consumption, higher inflation, and more pressure on businesses already dealing with affordability concerns.

Source: Bloomberg

#️⃣ #️⃣ #️⃣

#Finance #Oil #GasPrices #IranWar #EnergyMarkets #Inflation #StockMarket #Economy #Investing #Macro

The economic impact of the Iran war is now hitting American consumers directly at the pump.

US gasoline prices have climbed to around $4.56 per gallon, the highest level since July 2022, according to AAA data reported by Investopedia. Prices have risen for 15 consecutive days, jumping roughly 54 cents since April 22.

The pressure is not just on drivers.

Higher fuel costs act like a hidden tax on the economy: consumers spend more on gas, leaving less money for restaurants, retail, travel, and discretionary purchases.

• Higher gas prices can weaken consumer spending

• Transport and logistics costs may rise

• Inflation pressure could remain sticky

• Businesses dependent on discretionary spending may feel the squeeze

• Oil and energy stocks could benefit, while consumer-facing sectors face pressure

The conflict is also affecting global oil markets and shipping risk, especially around the Strait of Hormuz, one of the world’s most important energy chokepoints. AP reported fresh military tensions involving Iranian attacks on US Navy ships in the Strait of Hormuz, adding another layer of risk to energy markets.

This is bigger than expensive gas.

If energy prices stay elevated, the Iran war could become a macro problem: weaker consumption, higher inflation, and more pressure on businesses already dealing with affordability concerns.

Source: Bloomberg

#Finance #Oil #GasPrices #IranWar #EnergyMarkets #Inflation #StockMarket #Economy #Investing #Macro

Please open Telegram to view this post

VIEW IN TELEGRAM

{kind=link}

👏7🔥5❤3🎉3💯3👍1

For years, society promised that degrees and office jobs meant long-term security.

Now AI is beginning to challenge that assumption at scale.

The first wave is hitting:

📞 customer service

⚖️ legal support work

📊 junior finance roles

💻 entry-level coding

📑 administrative tasks

📈 consulting research work

Many companies are no longer asking:

“How do we hire more juniors?”

They’re asking:

“How many humans do we still need?”

A growing number of firms are using AI to automate:

• report generation

• document analysis

• customer interactions

• internal research

• data processing

• coding assistance

The biggest structural problem may not even be layoffs themselves.

It’s the collapse of the career ladder.

If AI removes junior and internship-level positions:

Unlike previous automation waves that mainly affected physical labor, this one directly targets cognitive and office-based work including jobs traditionally considered “safe.”

At the same time, AI will likely create entirely new industries and roles.

But transitions of this scale are rarely smooth.

The next few years could redefine:

🎓 higher education value

🏢 corporate hiring models

💼 white-collar employment

📉 wage structures

🌍 economic inequality

The question is no longer whether AI will affect white-collar work.

It’s how fast institutions can adapt before millions of careers are disrupted.

🎥 Source discussed:

How AI is Causing a White Collar Purge

#AI #Jobs #Economy #Automation #Finance #Technology #Careers #FutureOfWork #Layoffs #ArtificialIntelligence

Please open Telegram to view this post

VIEW IN TELEGRAM

YouTube

How AI is Causing a White Collar Purge

A generation was told that degrees meant security. Now those same jobs are disappearing, fast.

From finance and law to tech and consulting, AI is quietly replacing the very roles that once defined white-collar careers. Entry-level positions are vanishing…

From finance and law to tech and consulting, AI is quietly replacing the very roles that once defined white-collar careers. Entry-level positions are vanishing…

❤13💯10🎉7🔥6👍5👏3

Rising oil prices are putting pressure on low-cost carriers like JetBlue and Frontier, according to Bloomberg and Deutsche Bank analyst Michael Linenberg.

Higher fuel costs + weaker demand from budget-conscious travelers could lead to:

• more airline partnerships

• joint ventures

• possible mergers

👉🏻 The low-cost airline sector is becoming increasingly difficult to sustain independently as energy prices rise.

#Markets #Airlines #Oil #Finance

Please open Telegram to view this post

VIEW IN TELEGRAM

Bloomberg.com

Low-Cost Airlines ‘Ripe’ For Mergers, Deutsche Bank Analyst Says

The US airline industry is primed for a new round of mergers as low-cost carriers are squeezed by the oil-price spike, according to Deutsche Bank analyst Michael Linenberg.

👏6🎉6💯6❤5👍5🔥5

Ryan Cohen, GameStop, Nvidia, AI stocks, semiconductors, and fast food winners are all telling the same story:

Markets are still hunting for growth, but investors are becoming much more selective.

Ryan Cohen reportedly tried to push for a major move involving eBay, but the bid was rejected.

This matters because Cohen has built his reputation around activist investing, turnaround stories, and bold strategic changes. His role at GameStop already made him one of the most watched figures in retail investing.

But the rejected eBay bid shows a key limit:

even high-profile investors cannot force a deal when the target company does not see enough strategic value.

GameStop is still trying to find its next real business model.

The company has cash, brand recognition, and a loyal investor base, but the core gaming retail business remains structurally difficult. Physical game sales are weaker, digital distribution keeps growing, and the company still needs a convincing long-term growth engine.

📌Why it matters:

GameStop is no longer just a meme stock story.

It is now a test of whether a company with a strong balance sheet but a challenged business model can reinvent itself before investor patience fades.

The market is asking a simple question:

What is GameStop actually becoming?

AI stocks continue to dominate the market narrative.

Investors are still pricing in massive growth from AI infrastructure, chips, cloud computing, data centers, and enterprise adoption.

But when a theme becomes too obvious, risks increase.

AI is real.

The revenue growth is real.

The infrastructure demand is real.

But that does not mean every AI-related stock deserves any valuation.

This is where markets become dangerous:

a strong long-term trend can still create short-term bubbles.

Nvidia earnings matter because Nvidia has become the central stock of the AI trade.

Its results are not just about one company anymore.

They are a signal for the entire AI ecosystem: semiconductors, cloud providers, data centers, software companies, and even the broader Nasdaq.

If Nvidia beats expectations, the AI trade may keep running.

If guidance disappoints, the whole sector could reprice quickly.

Nvidia is now acting like a market thermometer.

Strong numbers confirm that AI infrastructure spending is still accelerating.

Weak numbers would raise doubts about whether expectations have moved too far ahead of reality.

Chip stocks continue to move aggressively higher as investors bet on AI demand, advanced computing, memory, networking, and data center expansion.

The semiconductor sector is no longer just cyclical.

It is becoming one of the core infrastructure layers of the global economy.

Semiconductors are the new oil of the AI economy.

But after such strong moves, investors need to separate real winners from hype-driven names.

The best companies have pricing power, supply advantages, strong margins, and exposure to real AI demand.

The weaker ones may simply be rising because the whole sector is hot.

Even with pressure on consumers, some fast food brands continue to perform well.

The winners are usually companies with strong pricing power, loyal customers, efficient operations, and menus that still feel affordable compared to full-service restaurants.

#Finance #StockMarket #Investing #Nvidia #AIStocks #Semiconductors #GameStop #eBay #RyanCohen #Markets #WallStreet #TechStocks #ConsumerStocks #FastFood #MarketNews

Please open Telegram to view this post

VIEW IN TELEGRAM

👏5🎉5👍4❤3💯3🔥2

🇺🇸 Fed Shock: Kevin Warsh Confirmed as New Fed Chair

The US Senate has confirmed Kevin Warsh as the next Chair of the Federal Reserve in a narrow 54-45 vote.

It was one of the most controversial Fed confirmations in modern history, with only one Democrat John Fetterman voting with Republicans.

Warsh will replace Jerome Powell at a very delicate moment:

inflation is rising again, long-term Treasury yields are back near crisis-era levels, and Donald Trump is openly pushing for lower interest rates.

That creates a dangerous policy dilemma.

The White House wants easier financial conditions.

Markets want inflation under control.

The Fed is supposed to remain independent.

The Fed Chair is one of the most important people in global finance.

Every signal from Warsh will now be watched by bond markets, equity investors, banks, hedge funds, pension funds, and foreign governments.

If investors believe the Fed is becoming politically influenced, confidence in US monetary policy could weaken.

That could push long-term yields higher, increase volatility, and make borrowing more expensive across the economy.

US investors bought 30-year Treasuries at yields above 5% for the first time since 2007.

This is a major signal from the bond market.

Higher long-term yields usually mean investors want more compensation for inflation risk, fiscal risk, or uncertainty about future interest rates.

In this case, the pressure is coming from several directions:

• rising energy prices

• renewed inflation fears

• weak demand for long-duration bonds

• concerns over Fed independence

• uncertainty around the Iran war

A 5% long bond changes the investment landscape.

When investors can get around 5% from long-term US government debt, risk assets need to justify much higher valuations.

That puts pressure on:

• growth stocks

• real estate

• private equity

• highly leveraged companies

• speculative tech names

Cheap money is no longer guaranteed.

Producer prices reportedly rose 6% year-over-year, the fastest pace since 2022.

This matters because producer inflation often feeds into consumer prices later.

If companies pay more for energy, materials, transport, and production, they may eventually pass those costs to consumers.

The problem for the Fed is simple:

Cutting rates could support growth and markets.

But cutting too soon could make inflation worse.

Sources:

#Finance #Markets #FederalReserve #Fed #KevinWarsh #JeromePowell #Trump #Inflation #TreasuryYields #Bonds #InterestRates #China #RareEarths #IranWar #Macro #Investing #StockMarket #WallStreet

Please open Telegram to view this post

VIEW IN TELEGRAM

Reuters

Warsh clinches Senate approval to be Fed's next chair as inflation intensifies

The vote was 54-45 in the most-partisan-ever Senate confirmation of a Fed chair. A single Democrat, John Fetterman of Pennsylvania, voted with the Republican majority.

JPY GDP QoQ Q1

Forecast: 0.4%

Previous: 0.3%

Japan’s GDP data will be watched closely because markets are still trying to understand whether Japan’s economy is strong enough to support further policy normalization.

Stronger growth could support the yen and increase expectations of tighter Bank of Japan policy.

A weaker number could reinforce the idea that Japan still needs caution before moving too aggressively.

GBP CPI YoY April

Forecast: 3.0%

Previous: 3.3%

UK inflation is expected to slow from 3.3% to 3.0%.

📌Why it matters:

If inflation falls as expected, it could strengthen the case for future Bank of England rate cuts.

If CPI comes in hotter than expected, markets may push back expectations for easing.

EUR CPI YoY April

Forecast: 3.0%

Previous: 3.0%

Eurozone inflation is expected to remain stable at 3.0%.

A stable CPI reading would support the view that inflation is not accelerating again, but it may not be enough to trigger a major repricing by itself.

The market reaction will depend on whether the number confirms a controlled inflation path or shows renewed pressure.

Previous: -4.306M

Oil inventories will be important for energy markets after the previous drawdown.

📌Why it matters:

Another large draw could support crude prices.

A surprise build could pressure oil lower, especially if demand concerns return.

Energy traders should watch this closely.

The FOMC minutes will be the main US macro event of the week.

📌Why it matters:

Markets will look for clues on how the Federal Reserve is thinking about inflation, labor market strength, financial conditions, and the timing of possible rate cuts.

The key question:

Is the Fed becoming more comfortable with easing, or still worried about inflation staying sticky?

Initial Jobless Claims

Forecast: 210K

Previous: 211K

Claims are expected to remain almost unchanged.

📌Why it matters:

The labor market remains central for Fed expectations.

If claims stay low, it suggests the job market is still resilient.

If claims rise sharply, markets may price in higher recession risk and faster rate cuts.

Forecast: 17.9

Previous: 26.7

The index is expected to slow from the previous strong reading.

📌Why it matters:

A weaker number could suggest cooling manufacturing momentum.

A stronger print would support the idea that US economic activity remains firm.

Manufacturing PMI

Forecast: 53.6

Previous: 54.5

Services PMI

Forecast: 51.1

Previous: 51.0

Both readings are expected to remain in expansion territory.

📌Why it matters:

PMIs are useful because they give a fast read on business activity.

Manufacturing is expected to slow slightly, while services are expected to remain stable.

If both surprise higher, risk assets may get support.

If both weaken, markets may worry about growth momentum.

German GDP QoQ Q1 will close the week for European macro watchers.

📌Why it matters:

Germany remains the largest economy in the Eurozone.

A weak GDP print would reinforce concerns about European growth.

A stronger number could support EUR sentiment and improve confidence in the region.

#Finance #Markets #Macro #Economy #FOMC #Inflation #CPI #GDP #PMI #Oil #FederalReserve #ECB #BankOfEngland #Japan #Germany #StockMarket #Forex #Trading

Please open Telegram to view this post

VIEW IN TELEGRAM

❤1

For decades, a degree was sold as a near-guaranteed path to stability. That assumption is breaking down.

Several forces are colliding:

🤖 AI & automation

Entry-level tasks in coding, marketing, analysis, customer support, and administration are increasingly automated. Companies may need fewer junior employees while expecting higher productivity.

🏢 Corporate culture shift

Firms are cutting training costs and increasingly want “job-ready” candidates with experience — even for so-called entry-level roles.

📉 Slower hiring market

Many sectors hired aggressively after COVID and later pulled back. Hiring rates remain weak despite low unemployment. Graduates face growing competition and underemployment.

🎯 Degree ≠ market demand

Universities often move slower than industry. Some graduates leave with credentials but without the specific skills employers need.

⚠️ Potential long-term risks:

• More graduates working outside their field

• Rising underemployment

• Higher pressure to pursue multiple degrees/certifications

• Greater inequality between adaptable workers and everyone else

• Growth of freelancing, startups, and self-employment paths

🎥 Full discussion: https://youtu.be/2PSnaEzRtrk

#Jobs #AI #Economy #Career #Finance #College #ArtificialIntelligence

Please open Telegram to view this post

VIEW IN TELEGRAM

YouTube

What Happens if Entry Level Jobs Don’t Exist Anymore

🚨 We're Hiring! If you like economics and want to be part of the creative process email theinvisiblehandyt@gmail.com

📊 Business Enquiries - theinvisiblehandyt@gmail.com

📊 Business Enquiries - theinvisiblehandyt@gmail.com

❤3💯3🔥2👏2🎉2👍1

🇺🇸🇨🇳 Why US–China Trade Talks Keep Failing

Another summit. Another round of handshakes. Little progress.

The deeper issue may not be tariffs or negotiations, but structural imbalances built into both economies.

Key idea:

📊 Trade deficits and surpluses are often driven by savings and investment patterns, not simply by trade policy.

China:

• High savings rates

• Lower household consumption relative to output

• Growth model historically tied to investment and exports

United States:

• Strong consumption-driven economy

• Persistent demand absorbing global production

• Role as the world’s “consumer of last resort”

The result?

⚠️ Tensions become difficult to solve through tariffs or diplomatic meetings alone because the incentives inside each economy remain unchanged.

This raises a bigger question:

Can the US–China economic conflict truly be resolved… or is it a structural feature of the global system?

Understanding these imbalances matters more than following headlines.

📱 Full video

#️⃣ #️⃣ #️⃣

#Economy #China #USA #TradeWar #Investing #Finance #Markets

Another summit. Another round of handshakes. Little progress.

The deeper issue may not be tariffs or negotiations, but structural imbalances built into both economies.

Key idea:

China:

• High savings rates

• Lower household consumption relative to output

• Growth model historically tied to investment and exports

United States:

• Strong consumption-driven economy

• Persistent demand absorbing global production

• Role as the world’s “consumer of last resort”

The result?

This raises a bigger question:

Can the US–China economic conflict truly be resolved… or is it a structural feature of the global system?

Understanding these imbalances matters more than following headlines.

#Economy #China #USA #TradeWar #Investing #Finance #Markets

Please open Telegram to view this post

VIEW IN TELEGRAM

YouTube

What Trump's China Visit Actually Achieved.

Try Mammouth AI now at http://mammouth.ai

As Donald Trump and Xi Jinping wrap up their summit in Beijing with little more to show for it than a few awkward handshakes, the media is left wondering where the big breakthrough went. But as we explore in this…

As Donald Trump and Xi Jinping wrap up their summit in Beijing with little more to show for it than a few awkward handshakes, the media is left wondering where the big breakthrough went. But as we explore in this…

❤4🔥4👏4👍3🎉3💯3

📅 This Week’s Economic Calendar: Key Events Markets Are Watching

Markets face a heavy macro week with inflation data, central banks, GDP updates, and labor indicators.

🇺🇸 United States

• Tue: Consumer Confidence (May)

• Thu: GDP Q1 (2nd estimate)

• Thu: Core PCE Inflation → one of the Fed’s preferred inflation metrics

• Thu: Initial Jobless Claims

• Thu: Durable Goods Orders

• Fri: Goods Trade Balance

• Fri: Chicago PMI

🇪🇺 Europe

• ECB Financial Stability Review (Tue/Wed)

• ECB Press Conference (Wed)

• ECB meeting accounts (Thu)

• German CPI (Fri) → key for Eurozone inflation expectations

🇯🇵 Japan

• BoJ Core CPI (Tue)

• Tokyo CPI (Thu night)

• Industrial Production (Fri)

🇳🇿 New Zealand

🔥 RBNZ Interest Rate Decision (Tue)

* Monetary Policy Statement & Press Conference

🇦🇺 Australia

• CPI updates

• Capital Expenditure data

🛢 Commodities

• US Crude Oil Inventories

• API Oil Stocks

• Baker Hughes Rig Count

⚠️ Potential high-volatility events:

1. US Core PCE → impacts Fed expectations

2. US GDP revision → growth outlook

3. RBNZ rate decision → NZD volatility

4. ECB communications → EUR sensitivity

5. German CPI → European inflation signals

Expect increased volatility in:

$SPY $QQQ $DXY $EURUSD $GOLD $OIL

#️⃣ #️⃣ #️⃣

#EconomicCalendar #Stocks #Investing #Macro #Fed #ECB #Inflation #Finance

Markets face a heavy macro week with inflation data, central banks, GDP updates, and labor indicators.

🇺🇸 United States

• Tue: Consumer Confidence (May)

• Thu: GDP Q1 (2nd estimate)

• Thu: Core PCE Inflation → one of the Fed’s preferred inflation metrics

• Thu: Initial Jobless Claims

• Thu: Durable Goods Orders

• Fri: Goods Trade Balance

• Fri: Chicago PMI

🇪🇺 Europe

• ECB Financial Stability Review (Tue/Wed)

• ECB Press Conference (Wed)

• ECB meeting accounts (Thu)

• German CPI (Fri) → key for Eurozone inflation expectations

🇯🇵 Japan

• BoJ Core CPI (Tue)

• Tokyo CPI (Thu night)

• Industrial Production (Fri)

🇳🇿 New Zealand

🔥 RBNZ Interest Rate Decision (Tue)

* Monetary Policy Statement & Press Conference

🇦🇺 Australia

• CPI updates

• Capital Expenditure data

🛢 Commodities

• US Crude Oil Inventories

• API Oil Stocks

• Baker Hughes Rig Count

⚠️ Potential high-volatility events:

1. US Core PCE → impacts Fed expectations

2. US GDP revision → growth outlook

3. RBNZ rate decision → NZD volatility

4. ECB communications → EUR sensitivity

5. German CPI → European inflation signals

Expect increased volatility in:

$SPY $QQQ $DXY $EURUSD $GOLD $OIL

#EconomicCalendar #Stocks #Investing #Macro #Fed #ECB #Inflation #Finance

Please open Telegram to view this post

VIEW IN TELEGRAM